Perpetual futures and spot markets trade the same underlying assets but require fundamentally different infrastructure. Spot is a one-layer instrument: price and volume. Perpetual futures are a three-layer instrument — price, volume, and a continuously updating set of funding, margin, and liquidation parameters that your platform must handle in real time, without exception.

This article is for brokerage owners, dealing desk heads, and infrastructure architects evaluating whether their current stack can support both instrument types, or deciding how to extend it.

By the end you will know:

- Why perpetual futures require three data fields that don’t exist in spot markets

- How the funding rate mechanism introduces a cost and risk dimension that spot systems cannot model

- What your connectivity layer needs to serve both books reliably

One asset, two very different instruments

Perpetual futures were invented by BitMEX in 2016 to solve a specific problem: traditional futures expire, forcing traders to roll positions forward — a friction that neither retail traders nor market makers found particularly appealing in crypto’s always-on markets. The perpetual contract removed expiry entirely, replacing the convergence mechanism of quarterly settlement with a periodic cash transfer between long and short holders called the funding rate.

That design decision, elegant in its simplicity, created a derivative that now dominates the market it was built to track. In 2025, perpetual futures accounted for approximately 77% of all crypto exchange volume — roughly $62 trillion in annual notional against $19 trillion for spot. On Bybit, the ratio across BTC contracts runs at more than 12:1 in favour of perpetuals. Any brokerage claiming to address the full crypto market while supporting only spot is, by this measure, addressing less than a quarter of it.

The infrastructure implications of that dominance are not merely quantitative. Perpetuals require a different data model, a different risk engine, and — if you’re connecting to upstream liquidity providers — a different interpretation of what “a feed” actually contains.

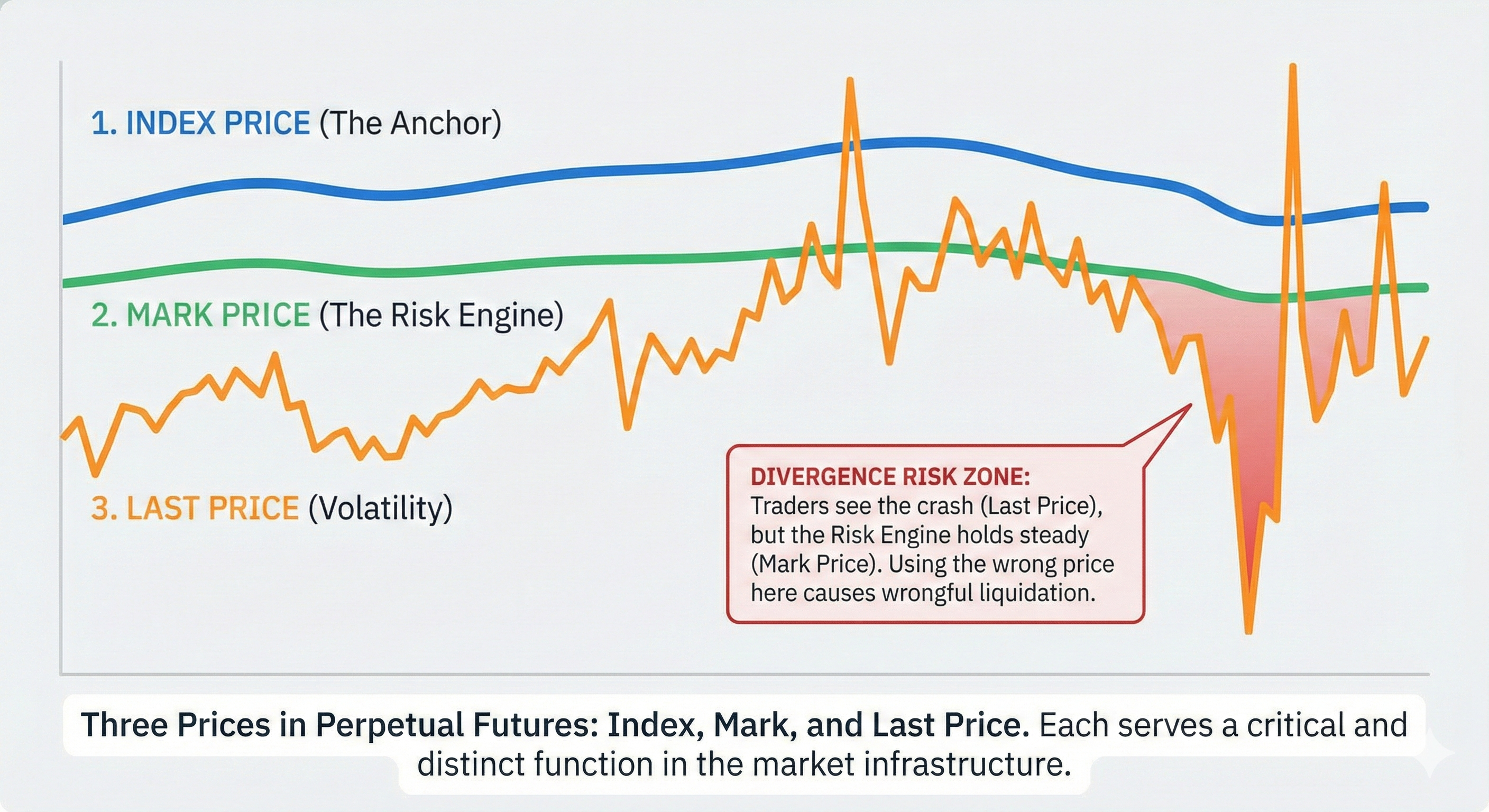

Three prices, not one

This is the first architectural divergence that catches teams off guard. In a spot market, one price does all the work: the last traded price (or mid-price between best bid and ask) determines value, drives P&L, and anchors risk calculations. In a perpetual futures market, three distinct prices operate in parallel, and confusing them produces incorrect P&L, misaligned margin calls, or worse — client positions liquidated on bad data.

Last price is the most recent execution on the perpetual order book. Traders use it to understand where the market is transacting, but it’s vulnerable to momentary illiquidity or manipulation on thin books.

Index price is a manipulation-resistant composite. It’s computed as a volume-weighted average of spot prices across six to eight major exchanges — typically Binance, Coinbase, Kraken, OKX, and others — with price caps applied when any single source deviates more than 5% from the median. It represents the best available estimate of the underlying asset’s “true” current value.

Mark price is the field that actually runs your risk engine. Computed by most venues as the median of two values derived from the index price and recent premium data, it is the price against which margin ratios are evaluated and liquidations are triggered. A client gets liquidated at mark price, not last price — and that distinction matters precisely when the two diverge most: during volatility spikes, when last price can flash 3–5% away from mark price in seconds.

For every perpetual symbol your platform distributes, mark price must accompany the quote. It’s not supplementary market data — it’s load-bearing infrastructure.

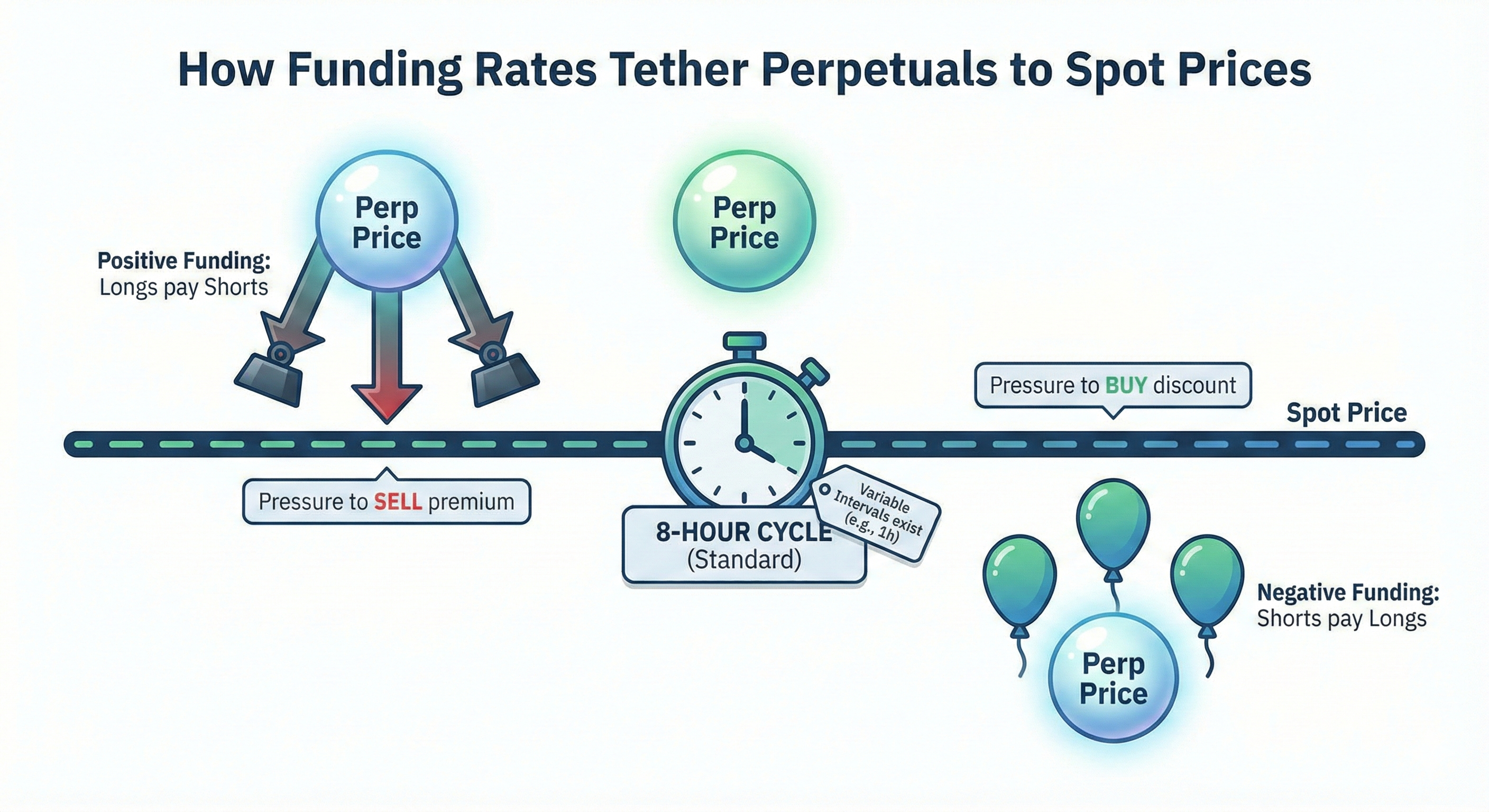

The funding rate: the mechanism that holds it all together

The funding rate is what prevents perpetual futures from drifting permanently away from spot. Every eight hours — at 00:00, 08:00, and 16:00 UTC on most major venues — a cash transfer occurs directly between long and short position holders. When the perpetual trades above the spot index, longs pay shorts, creating economic pressure to sell down the premium. When it trades below, shorts pay longs, encouraging buyers. The exchange takes no cut.

At the typical rate of 0.01% per eight-hour interval, this amounts to roughly 10.95% annualised — material but manageable. During bull market phases when speculative demand crowds into long positions, funding can spike to 0.1% per interval or higher, implying more than 100% annualised. In bear markets the rate inverts: shorts pay longs.

For a brokerage’s dealing desk, this dynamic is simultaneously a revenue source (a hedged long-spot/short-perp position earns positive carry when funding is elevated) and a risk factor (rates are not fixed; a position entered at 0.05% per interval can face negative funding within the same trading session if sentiment reverses).

The operational implication: every perpetual symbol your platform distributes needs to carry the current funding rate and the funding interval alongside the quote. A system that assumes all perpetual contracts settle every eight hours will miscount funding exposure on venues like Kraken, which settles every four hours — a twofold error in position cost calculations. The interval must be a per-symbol field, not a global constant.

Margin, leverage, and the liquidation engine

Unless an exchange offers spot margin (borrow-and-trade), classical spot trading has no margin, no leverage, and no liquidation logic. The worst outcome for a spot holder is that the asset price goes to zero. Perpetual futures add all three, and each creates real-time obligations your platform must monitor continuously.

Initial margin is the minimum collateral required to open a position. At 20x leverage, that’s 5% of notional. Maintenance margin is the lower threshold — typically around 0.4–0.5% of notional at the top tier — below which the position is liquidated. The gap between the two is the buffer zone.

When margin equity falls below the maintenance threshold — measured against mark price — the exchange’s liquidation engine activates. Most venues run a staged process: warning, partial reduction, then full liquidation. If the liquidation fills better than the theoretical bankruptcy price, the surplus flows to an insurance fund. If it fills worse, the fund covers the deficit. When that fund runs dry, auto-deleveraging (ADL) triggers: the most profitable opposing positions are forcibly reduced without warning.

This is not theoretical edge-case risk. Cascading liquidation events occur regularly in crypto markets, moving billions of notional in minutes. A brokerage infrastructure that cannot surface insurance fund levels and mark-price-based margin ratios in real time is operationally blind during the periods that matter most.

The second design choice — cross-margin versus isolated margin — compounds the complexity. Cross-margin nets all positions against a shared collateral pool; isolated margin quarantines each position independently. Both modes must be supported. Institutional clients and market makers strongly prefer cross-margin for capital efficiency. Retail-facing platforms default to isolated for containment. Offering only one will either lose institutional flow or expose retail clients to unnecessary liquidation risk.

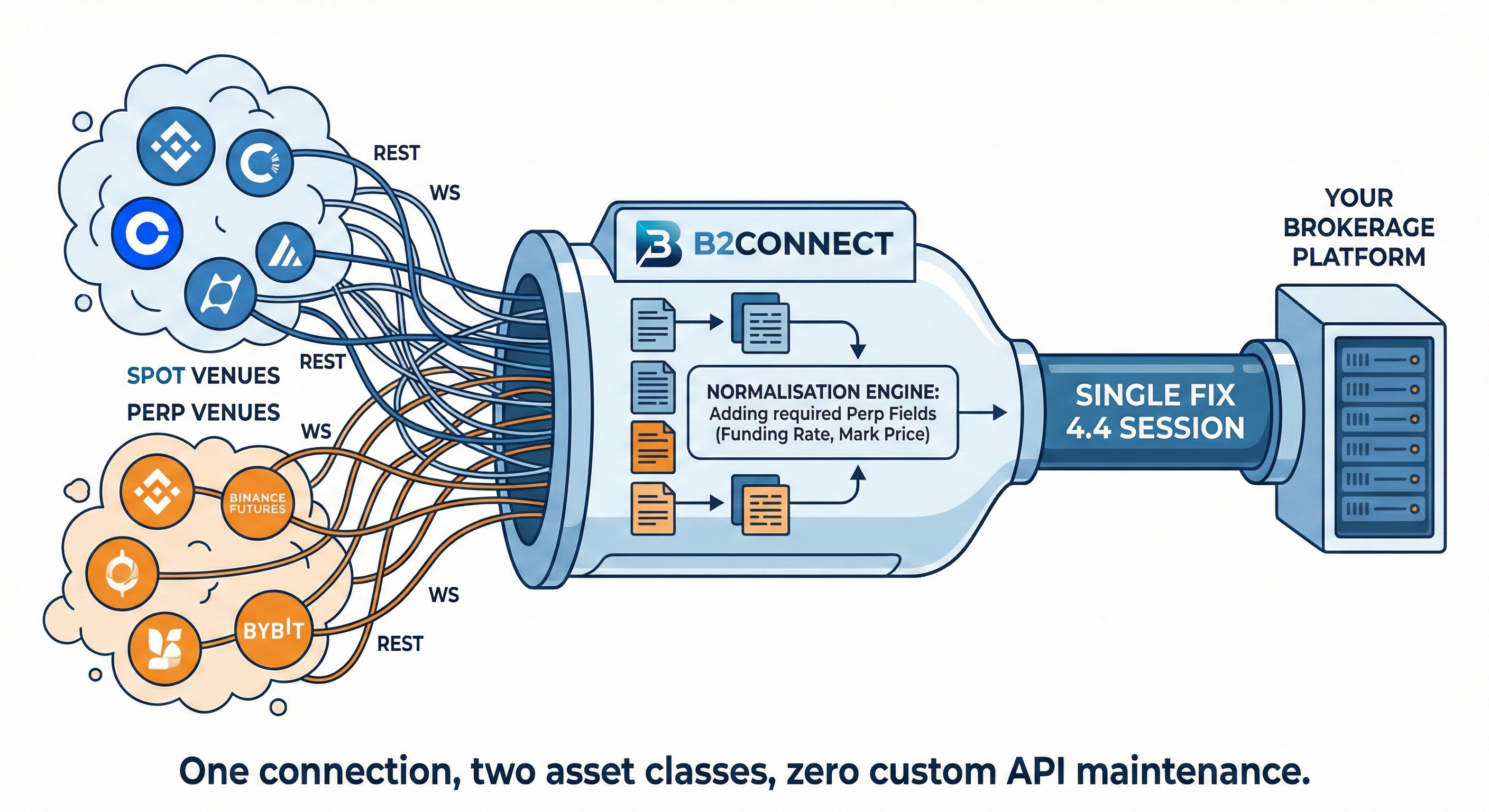

What your connectivity layer actually needs

The gap between “we support spot” and “we support both” is not bridged by a feature flag. It requires three concrete additions to your data and connectivity architecture.

First, your market data schema must carry the perpetual-specific fields for every symbol. Funding rate, mark price, and funding interval are not decorative metadata — they drive P&L display, margin calculations, and client-facing liquidation price estimates. A spot market data schema that carries only price and volume cannot model these instruments correctly, regardless of what happens further up the execution stack.

Second, your risk engine must reference mark price — not last price — for all margin and liquidation calculations. This requires that mark price be delivered to the risk layer in real time, updated continuously, not polled periodically.

Third, your connectivity to upstream venues must be able to source both spot and perpetual data reliably, with failover handling if a venue becomes unavailable. Perpetual futures venues are not an optional extension of spot connectivity — they are the primary volume venue for every major crypto asset.

On the protocol side, FIX 4.4 — the institutional standard for order routing and market data — does not natively include tags for funding rate, mark price, or funding interval. These require custom field extensions. Any aggregation layer claiming to deliver perpetual futures data over FIX must explicitly implement and document those extensions. Without them, a downstream platform connecting via FIX will receive well-formed messages that simply lack the fields needed to operate a perpetual book.

Dual-book hedging: opportunity and discipline

A brokerage that runs both spot and perpetual books acquires a hedging toolkit that spot-only operations simply don’t have. The classic structure is the basis trade: long spot, short the equivalent notional in perpetuals, collect positive funding. At a typical rate of 0.01% per eight-hour interval, a $10 million position earns roughly $3,000 per day — market-neutral, subject to basis and rate variability. During elevated funding phases — 0.05–0.10% per interval — the same structure generates $15,000–$30,000 daily. BIS research confirms crypto carry averages above 10% per annum and frequently exceeds 40% during trending market conditions.

The discipline comes in the edges. Funding rates are not locked in. A position initiated at a favourable rate can turn costly if rates invert within the same session. Basis — the spread between perpetual mid-price and spot mid-price — can widen unexpectedly during volatility, meaning the hedge performs differently from how it was modelled. And if the short perpetual leg is on isolated margin, it can be liquidated independently of the long spot position during a sharp upward move, crystallising a loss on a position that was supposed to be hedged.

Running both books well requires real-time mark-price-based P&L across all positions, per-symbol control over hedge ratios (some symbols should be fully hedged; others can be warehoused), and a reliable feed of funding rate data — not batch-polled, but delivered as part of the real-time market data stream.

FAQ

Does my existing FIX integration cover perpetual futures data, or do I need changes?

How do I normalise funding rates from venues that use different calculation formulas?

What’s the practical difference between cross-margin and isolated margin for my infrastructure?

How material is the latency impact of adding perpetual data fields to a FIX feed?

What is the regulatory direction for perpetual futures?

Do I need separate venue relationships for spot and perpetual futures?

Key Takeaways

- Perpetual futures are not leveraged spot. They require three additional data fields — funding rate, mark price, funding interval — and a margin and liquidation engine that spot-only infrastructure cannot provide.

- With perpetuals representing $61.7T (vs $18.6T) of crypto exchange volume in 2025, a spot-only brokerage is addressing less than a quarter of the market by notional activity.

- Mark price — not last price — is the operationally correct reference for margin calculations and liquidation triggers. Any system that conflates the two will produce incorrect P&L and potentially wrongful liquidations.

- Funding intervals vary by venue. Assuming all perpetuals settle every eight hours will introduce twofold errors in cost calculations for venues like Kraken that settle every four hours.

- Dual-book operations create a genuine carry opportunity — typically 6–20%+ annualised in normal to elevated funding conditions — but require per-symbol hedge ratio control and real-time funding rate data, not periodic polling.

B2CONNECT is a crypto-native liquidity hub built from the ground up for CEX spot and perpetual futures connectivity — and designed to extend cleanly into TradFi systems via FIX. To discuss how it fits your stack, request a technical conversation with the B2CONNECT team.

References

- TradingView / NewsBTC, “Futures Frenzy Pushed Crypto Exchange Volume To Nearly $80 Trillion In 2025”

- Bybit Help Center, “Mark Price Calculation (Perpetual Contract)”

- One Trading, “Understanding the Funding Rate in Perpetual Futures”

- BIS Working Papers No. 1087, “Crypto carry” (2023)

- Pillsbury, “CFTC Permits Listing of Perpetual Futures on BTC and ETH” (2025)

- B2CONNECT Documentation, “FIX API”

- B2CONNECT Release Notes, “Perpetuals data over FIX”

- B2CONNECT Documentation, “Supported Venues”

B2CONNECT Product Team · Last updated: February 2026